Company car taxation in Belgium

Table of contents

Introduction

The regulations concerning company cars are constantly changing, making it increasingly difficult to keep an overview. On this page, we provide a clear and concise overview of the taxation of company cars in Belgium and how it has evolved over the years.

For employers, the tax aspects of company cars are mainly important in two major areas: tax deductibility and the CO2 solidarity contribution. For employees, the Benefit in Kind (BIK) is the tax that is charged monthly via the payslip.

Tax deductibility

Tax deductibility determines to what extent the costs of a company car may be deducted from taxable profit. The higher the deductibility, the lower the taxable profit — and therefore the less corporate tax the company has to pay.

Non-deductible costs are referred to as disallowed expenses. These cannot be deducted from profit. The result? A higher tax burden.

The deductibility of car expenses mainly depends on:

the type of fuel (e.g. electric, hybrid, petrol or diesel);

the date of purchase or leasing, as this determines which tax regime applies.

Electric vehicles generally benefit from maximum deductibility, while high-emission cars are significantly less tax-advantageous. The government uses this mechanism to encourage more environmentally friendly vehicle use.

CO2 solidarity contribution

In addition to corporate tax, there is also the CO2 solidarity contribution, a mandatory employer contribution for every company car that is made available to an employee for private use.

This contribution also depends on:

the vehicle’s CO2 emissions;

the type of fuel.

The more polluting the car, the higher the contribution. For fully electric vehicles, a minimum contribution currently applies. In 2025, the contribution for electric cars amounts to €447.96 per year. This contribution is calculated monthly but paid quarterly to the NSSO, together with other social security contributions.

Benefit in Kind (BIK)

In Belgium, a benefit in kind must be paid when an employee is allowed to use a company car for private purposes. This benefit is considered additional taxable income because the employee receives an advantage outside of their salary. The BIK ensures that the private use of a company car is treated and taxed correctly.

Company cars ordered before 1 July 2023

Zero-emission vehicles

Electric (and hydrogen) company cars purchased or leased before 1 July 2023 remain 100% tax-deductible throughout their entire period of use. This advantage is retained regardless of how the legislation evolves after that date.

With regard to the CO2 solidarity contribution, the minimum amount applies, which is adjusted annually.

Non-zero-emission vehicles

For combustion engine or hybrid vehicles ordered before 1 July 2023, deductibility also remains unchanged throughout their period of use. It is determined using the existing formula:

Deduction percentage = 120% – (0.5 × fuel coefficient × CO2 emissions)

Fuel coefficient:

Diesel: 1.00

Petrol, LPG, hybrid, CNG (≥ 12 hp): 0.95

CNG (< 12 hp): 0.90

A fuel-efficient plug-in hybrid generally achieves deductibility between 95% and 100%, while an older high-emission diesel can fall to the minimum deductibility of 50%.

The CO2 solidarity contribution is calculated as follows:

Contribution = [(CO₂ emissions × €9) – 768 (petrol) or 600 (diesel) or 990 (LPG)] ÷ 12

The result is then adjusted based on the health index:

Adjusted contribution = contribution × (health index of the year of purchase ÷ 114.08)

The final monthly contribution is therefore indexed according to the year in which the car was purchased or leased. 114.08 is the index from September 2004, which always serves as the reference.

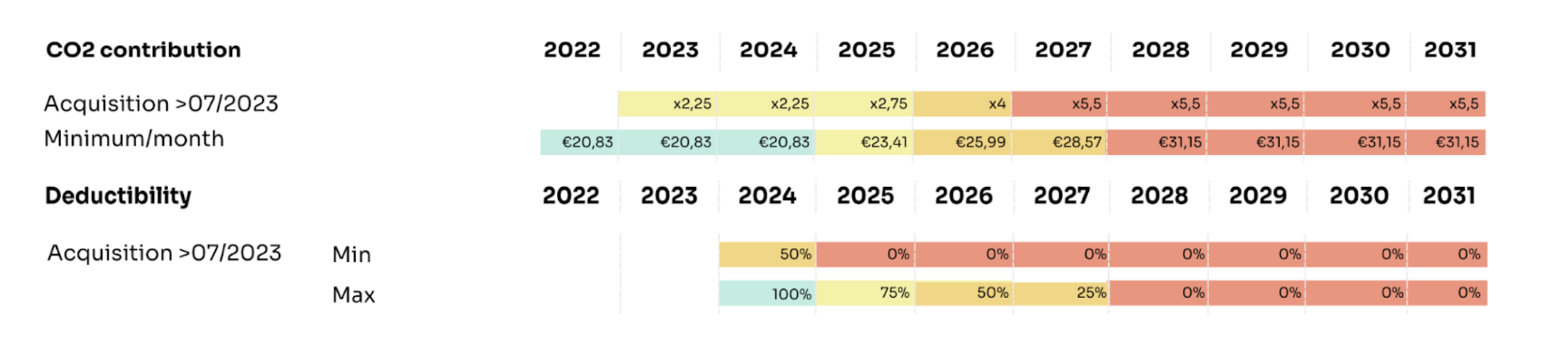

Company cars ordered from 1 July 2023

Zero-emission vehicles

Electric (and hydrogen) company cars ordered or leased from 1 July 2023 remain 100% tax-deductible until 31 December 2026. This means that all car-related costs are fully deductible from taxable profit, resulting in lower corporate tax. From 2027 onwards, this tax deductibility will be gradually phased out, reaching at least 67.50% in 2031.

As for the CO2 solidarity contribution: for electric vehicles, the minimum amount remains applicable.

Non-zero-emission vehicles

For company cars with emissions ordered after 1 July 2023, the tax framework changes significantly. Although the calculation method for deductibility (via the CO2 formula) remains, it is now subject to a phase-out schedule for both maximum and minimum deductibility:

Since 2025, the minimum deductibility is 0%, meaning that high-emission cars may become entirely non-deductible.

By 2028, the maximum deductibility will also be reduced to 0%, regardless of CO₂ value or fuel type.

A fuel-efficient plug-in hybrid may still enjoy deductibility of 95% to 100% in the early years, while a polluting diesel will quickly fall below 50%, and even close to 0%.

CO2 solidarity contribution: calculated largely as before 1 July 2023, but now subject to an (extra) multiplier. The formula mentioned earlier is therefore multiplied by an additional factor. In 2025, the result of the original formula is multiplied by 2.75, and in 2026 by 4. This means the NSSO contribution rises significantly over the years.

Company cars with emissions ordered from 2026 onwards will be immediately deductible at 0%, and will not follow the phase-out scedule. Ordering these vehicles in 2026 therefore does not seem to be a good idea.

Benefit in Kind (BIK)

The BIK for company cars is calculated based on three main criteria: the catalogue value of the car (including options and VAT, excluding discounts), the vehicle’s CO2 emissions, and the car’s age. The formula takes into account a CO2 coefficient, which increases the benefit as emissions rise, but with a cap to avoid excessive amounts. In addition, a depreciation percentage is applied depending on the number of years since the car’s first registration, meaning the BIK decreases as the car ages.

For electric cars, a fictitious CO2 emission of 0 g/km applies, which significantly lowers the BIK compared to combustion engines. The calculated benefit in kind may never be lower than the base amount of €820 per year, which is indexed annually. For 2025, this minimum amount is €1,650 per year, which is also the BIK for an employee with an electric company car.

Formulas for non-zero-emission cars:

- For diesel cars: catalogue value × [(5.5 + ((CO2 emissions – 59) × 0.1))%] × 6/7 × age coefficient

- For petrol, fake hybrid, LPG and CNG cars: catalogue value × [(5.5 + ((CO2 emissions – 71) × 0.1))%] × 6/7 × age coefficient

- For plug-in hybrid cars: catalogue value × 4% × 6/7 × age coefficient

Age coefficient:

- 0 to 12 months: 100%

- 13 to 24 months: 94%

- 25 to 36 months: 88%

- 37 to 48 months: 82%

- 49 to 60 months: 76%

- 61 months and more: 70%

Charging stations and charging costs

At the employee’s home

Charging stations installed at the employee’s home and financed by the employer are 100% deductible. For houses older than 10 years with a fixed charging station, a reduced VAT rate of 6% applies. For the employee, no additional BIK is due for the installation of the home charging station. The employee therefore does not need to declare this benefit in their tax return.

Employers may reimburse electricity costs for home charging of an electric or plug-in hybrid company car without creating an additional benefit in kind for the employee, provided certain conditions are met:

- The charging station must be located on the employee’s private property.

- The charging station must be equipped with a communication system that reports the electricity consumed to the employer.

- The reimbursement must be explicitly included in the employer’s car policy.

- The reimbursement may only relate to the electricity consumed for charging the company car provided.

Calculating the actual electricity costs for home charging is often complex. Many households only have a single electricity meter that records total consumption, without distinguishing between private use and car charging. In addition, consumption may vary depending on charging time, energy contract and charging station type. These factors make it time-consuming and administratively burdensome to calculate the actual costs. That is why the FPS Finance allows these electricity costs to be reimbursed based on the CREG tariff. The employer may choose to reimburse the employee based on the CREG tariff of the relevant region, or to reimburse all employees based on the lowest CREG tariff of the three regions.

Current CREG tariffs:

- Flanders: €0.3456/kWh

- Brussels: €0.3787/kWh

- Wallonia: €0.3843/kWh

At the office

Charging stations installed at the office are 100% deductible until 2029. From 2030 onwards, deductibility will decrease to 75%. The following conditions must always be met:

- It must be a new charging station;

- It must be accessible to the public*;

- It must be smart: charging time and power must be controllable via an energy management system.

* The charging infrastructure must be freely accessible, at least during or outside the company’s normal opening hours.

Are you in the process of electrifying your fleet? Or are you now convinced to do so? Then take a look at our Mbrella Charge Module.

Avoid the hassle of finding the right formula for your TCO.

With our free TCO Calculator template you can start calculating your mobility budget in no-time.

Related content

Data in Fleet Management Guide 2026

20% total gross wage calculator

Ready to try our product?

Start offering flexible and green mobility to your employees without the burden of administrative hassle. Get in touch for a full demo of our platform or sign up for a free account.

FAQs

Every question has an answer. Can't find the answer to your question? Let us know!

The mobility budget is based on the total gross cost of the employer to provide a company car to the employee for one year. The law allows two methods to calculate the TCO. TCO2 is always the starting point used to calculate the mobility budget. A more complete overview of the two methods can be found here.

- Depending on the expenditure taxes and social contributions are paid.

- Commute expenses for parking, bike and public transport are tax and social contribution free.

- Commute expenses for other mobility services are not tax free, this can influence personal tax income (employee) & company tax (employer). But are social contribution free.

- Mobility Expenses for private reasons are handled like it is gross wage.

Mbrella has created the first corporate mobility solution that is designed to empower employees while unburdening mobility professionals completely. Mbrella enables employees to compose their ideal mobility mix, tailor their own salaries, track their mobility spend and check their EV charging status on the go. For employers, Mbrella lets you put your entire mobility policy on auto-pilot. From automated expense approvals and kilometer allowances to pre-paid payment cards, self-service public transport orders and custom EV charging budgets, Mbrella takes the hassle out of flexible and sustainable mobility. On top of that, everything is smoothly integrated with your payroll provider to ensure the most correct payslip you’ve ever seen. Fair & flexible compensation, with no admin.

Mbrella is the first corporate mobility solution that is designed to empower employees while unburdening HR professionals completely. Mbrella enables employees to compose their own ideal mobility mix and monitor their allocated budget on the go through an intuitive mobile app. Our integration with your payroll provider ensures correct remuneration. Fair & flexible compensation packages with no admin, what’s not to like? On top of that, you can track the total impact of your company’s efforts with our Carbon Tracker.

Employees can spend the federal mobility budget on various options. These include eco-friendly cars, sustainable transport like bicycles and public transport, and housing costs within a certain distance from work, or are working from home more than half of the time. Additionally, any remaining budget can be received in cash at a favorable tax rate, ensuring flexibility and tax efficiency. Read more here: https://app.mbrella.io/explore-hub

To correctly calculate the Total Cost of Ownership (TCO) for the Belgian mobility budget, include all costs related to the company car such as purchase or lease price, fuel, insurance, maintenance, taxes, and depreciation. This calculation can use actual costs or a lump-sum formula, ensuring all relevant expenses are considered over a four-year reference period.

The Federal mobility budget is a flexible system allowing employees to exchange their (right to a) company car for a budget. This budget can be spent on eco-friendly cars, sustainable transport options, and housing costs. Unused budget can be received as cash at the end of the year at a favorable tax rate. This offering tax benefits and promoting sustainable mobility.